Most people who own a health insurance policy carry a quiet sense of financial security about their medical future. They’ve done the responsible thing — they’ve insured themselves. If something goes wrong, they’re covered. That belief is largely correct for a wide range of medical situations. But there is a specific category of serious illness where standard health insurance falls significantly short, and the gap it leaves can be financially devastating for a family even when the treatment itself is covered.

That gap is precisely what critical illness cover is designed to fill. And understanding the difference between the two products — not just what they cover, but how they pay and when — is one of the most important insurance decisions an earning individual can make.

What Health Insurance Actually Does

A standard health insurance policy — whether individual or family floater — is fundamentally a hospitalisation reimbursement product. It pays your hospital bills. When you are admitted, undergo surgery, receive treatment, and are discharged, your insurer settles the medical expenses either directly with the hospital through cashless claims or reimburses you afterwards.

This is genuinely valuable and essential. But notice what it covers and, more importantly, what it doesn’t. It covers the cost of treatment. It does not cover the cost of recovery. It does not replace lost income during months of inability to work. It does not fund lifestyle modifications required after a major diagnosis. It does not pay your EMIs while you’re bedridden. It does not cover the experimental treatments or international consultations that fall outside the policy’s approved list.

For a routine hospitalisation — a fracture, an appendectomy, a delivery — health insurance is sufficient. For a life-altering diagnosis like cancer, a heart attack, or a stroke, health insurance addresses only one part of a much larger financial crisis.

What Critical Illness Cover Does Differently

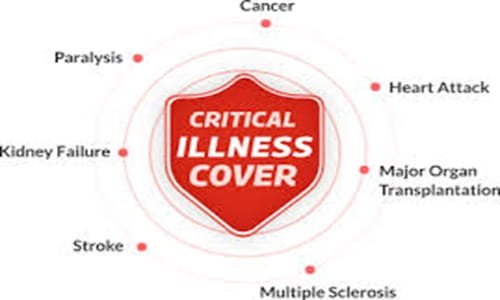

A critical illness policy works on an entirely different principle. It is a benefit-based product rather than a reimbursement-based one. When you are diagnosed with one of the listed critical illnesses — typically including cancer of specified severity, first heart attack, stroke, kidney failure, major organ transplants, coronary artery bypass surgery, and several others — the insurer pays you a pre-agreed lump sum amount regardless of what you actually spend on treatment.

You receive the full sum insured in a single payment. No bills required. No hospitalisation receipts. No room rent limits or sub-limits on specific procedures. The money arrives in your bank account, and how you use it is entirely your decision.

This distinction is transformative in practice. A critical illness payout of ₹25 lakh doesn’t just cover your chemotherapy bills — it can replace six months of lost income, clear your home loan EMIs, fund post-treatment rehabilitation, allow your spouse to take leave from work to care for you, and cover the hundred smaller expenses that never appear on a hospital invoice but are just as real.

The Income Replacement Problem Health Insurance Doesn’t Solve

This is the dimension of critical illness that most people haven’t thought through until it’s too late.

When a 42-year-old primary earner is diagnosed with cancer and undergoes treatment over eight months — surgery, chemotherapy, radiation, recovery — the family’s income can drop to zero or near-zero during that entire period. The EMI on the home doesn’t pause. The children’s school fees don’t pause. The household expenses don’t pause.

Health insurance, however comprehensive, does not address this dimension at all. It was never designed to. A critical illness lump sum, on the other hand, can serve as an income bridge — not just paying the medical bills that health insurance might cover anyway, but sustaining the family’s financial life during a period of genuine crisis.

The Overlap Question — Are You Paying for the Same Thing Twice?

A common and entirely reasonable concern is whether buying both health insurance and critical illness cover creates redundant, overlapping coverage. The answer is no — and the reason lies in how differently the two products respond to the same diagnosis.

Suppose you are diagnosed with a heart attack and spend ₹8 lakh in hospital treatment. Your health insurance settles the ₹8 lakh hospital bill directly. Your critical illness policy simultaneously pays you ₹25 lakh as a lump sum benefit. Both claims are valid and paid independently. The critical illness payout is not reduced by what your health insurance covered — the two products respond to the same event in different ways, solving different problems.

There is no duplication. There is complementarity. Health insurance covers the treatment cost. Critical illness cover funds everything else.

What to Look For in a Critical Illness Policy

Not all critical illness policies are equal, and the fine print matters more here than almost anywhere else in insurance.

The number of illnesses covered varies significantly — some basic plans cover eight conditions while comprehensive plans cover 30 or more. Check whether cancer is covered at early stages or only at advanced stages. Some policies exclude the first 90 days after policy inception for critical illness claims — this initial waiting period means a diagnosis in the first three months won’t trigger the benefit. The survival period clause — requiring the insured to survive a minimum number of days after diagnosis, typically 30 days, to receive the payout — is another detail worth reading carefully.

Sum insured selection matters enormously. Given that the lump sum must cover income replacement, loan obligations, and lifestyle costs beyond just medical bills, a sum insured of at least ten to fifteen times your monthly income is a reasonable planning benchmark.

Who Needs Critical Illness Cover Most Urgently

The product is relevant across age groups but becomes increasingly critical with age. For individuals between 35 and 55 who carry significant financial obligations — home loans, dependent parents, school-going children, business liabilities — a critical illness diagnosis without a lump sum cover can unravel years of financial planning in a matter of months.

Family history of heart disease, cancer, or diabetes elevates the urgency further. Premiums for critical illness cover are significantly lower when purchased at younger ages, making early purchase not just prudent but financially smart.

Salaried employees who lose income during extended medical leave and self-employed individuals with no employer-provided sick pay are the most exposed to the income replacement gap that critical illness cover addresses.

Frequently Asked Questions (FAQs)

Q1. Can I claim both my health insurance and critical illness policy for the same illness?

Yes, absolutely. These are two separate insurance products that respond to the same illness in different ways. Your health insurance settles hospitalisation expenses through cashless or reimbursement mode. Your critical illness policy pays the lump sum benefit upon diagnosis, independent of what your health insurance covers. Both claims are valid simultaneously, and accepting one does not affect the other.

Q2. Is critical illness cover available as a rider on an existing health or life insurance policy?

Yes. Many life insurance and health insurance policies offer a critical illness rider at an additional premium. The advantage is simplified administration — a single policy and premium payment. The limitation is that riders typically offer lower sum insured amounts and cover fewer illnesses than a standalone critical illness policy. For individuals who need comprehensive coverage, a dedicated standalone critical illness policy is usually more thorough than a rider.

Q3. What happens if I am diagnosed with a critical illness but survive for fewer than the required days under the survival clause?

Most critical illness policies include a survival period of 30 days from the date of diagnosis. If the insured passes away within this period, the critical illness benefit is typically not paid. The reasoning is that the product is designed for managing the long-term financial consequences of surviving a serious illness, not as a death benefit. Life insurance serves the latter purpose. This is why having both life insurance and critical illness cover is part of a complete financial protection plan.

Q4. Are pre-existing critical illnesses covered under a new critical illness policy?

No. Pre-existing conditions are typically excluded from critical illness cover, similar to health insurance. Most policies also include a waiting period of 90 to 180 days during which no claim can be made for a newly diagnosed critical illness. If you already have a diagnosed critical illness at the time of policy purchase, that specific condition will almost certainly be excluded from coverage.

Q5. How does the premium for critical illness cover change with age?

Critical illness premiums increase significantly with age because the probability of diagnosis rises sharply as you grow older. A ₹25 lakh critical illness cover might cost ₹3,000 to ₹5,000 annually at age 30, but the same cover could cost ₹15,000 to ₹25,000 or more at age 50. Purchasing early locks in lower premiums for a longer period and ensures coverage is in place before health deterioration makes the product either unaffordable or unavailable.